Plenty of guidance exists for businesses regarding whether they should lease or buy, but there is not much out there for businesses looking to lease out vs. loan. This article, and corresponding excel tool, explores the differences between leasing out an asset vs. financing its purchase to a customer through a loan.

See all the details of impacts for your specific case with our calculator.

Considerations of leasing an asset (from a lessor’s perspective)

1. Future use

a. Assuming “operating” classification, the leased asset will eventually be returned to you by the lessee, and you will be able to again lease out the asset or sell it or use it as you otherwise desire.

2. Income

a. You enjoy the monthly income that you receive like that of a loan.

3. Depreciation expense

a. Under ASC 842, when classified as an operating lease, the lessor keeps the asset on their books and continues to depreciate it over the useful life of the asset.

b. Depreciation is a non-cash expense, and it can, therefore, impact your business in many ways, but it will lower your overall bottom line.

4. Default risk

a. With leases, there is also a much lower risk for default, because the asset will return to you if the lease payments are not made.

Considerations of financing an asset purchase

1. Future use

a. Because you no longer own the asset, you won’t have any use of it in the future unless you repurchase it, whereas with an operating lease, the asset would eventually return to you.

2. Income

a. When selling an asset and financing its purchase via a loan, you will enjoy the benefits of receiving a monthly payment.

b. A large portion of this monthly payment, especially at the beginning, will be allocated to interest income.

3. Depreciation expense

a. When you remove the asset from your books, you will no longer record depreciation.

4. Default risk

a. One possible downside to financing an asset purchase via a loan is that there is a much higher risk of default.

b. This risk can of course be mitigated through the proper KYC procedures; however, the risk remains and if your customer cannot pay, there is a chance you will be left unpaid and without your asset.

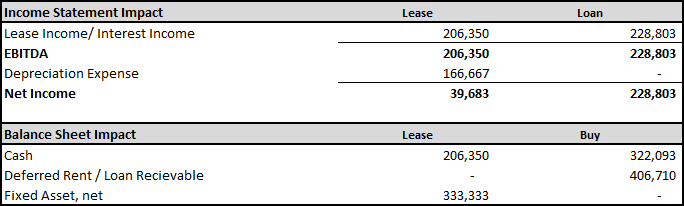

FS implications

Let's review and highlight the key similarities and differences in the accounting.

Balance-sheet impact

On the balance sheet, both will receive cash on a monthly basis. The leased asset will remain on the books along with accumulated depreciation, while it will be completely removed with the loan. The loan will also retain a loan-receivable asset on the books for the life of the loan.

Income-statement impact

On the income statement, both leasing and loaning will recognize revenue on a monthly basis. A lease will keep the asset on books and continue depreciating it throughout its useful life, whereas a loan would remove the asset from the books entirely.

Explore these impacts with our calculator tool:

Bottom line

Ultimately, it comes down to your business and what your long-term goals are. If you want to lower your overall net income to take advantage of certain tax situations, leasing is the way to go. If you are looking for a higher EBITDA, loaning would likely be more advantageous. See the visual below for the full accounting impact. You can also download a lease vs. loan calculator here to change the assumptions and see the accounting impact your leases/loans have on your financial statements.

|

Lessor assumptions Lease classification: Operating Commencement date: 1/1/2022 Lease term: 120 months Payment timing: In arrears Monthly lease payment: $1,500 with 3% annual increases |

Purchase/Loan assumptions Purchase Price: $500,000 APR: 5% Payment timing: In arrears Monthly loan payment: $2,684 Loan Life: 360 months |

Financial Statement impact after 10 years (as of 12/31/2031):