When I was a tax senior associate at a big-four accounting firm, depreciation was the book-to-tax adjustment that I dreaded the most. The tax depreciation computation itself is easy. But aligning client provided book asset information with the tax asset information stored on our in-house software was manual, tedious and time-consuming.

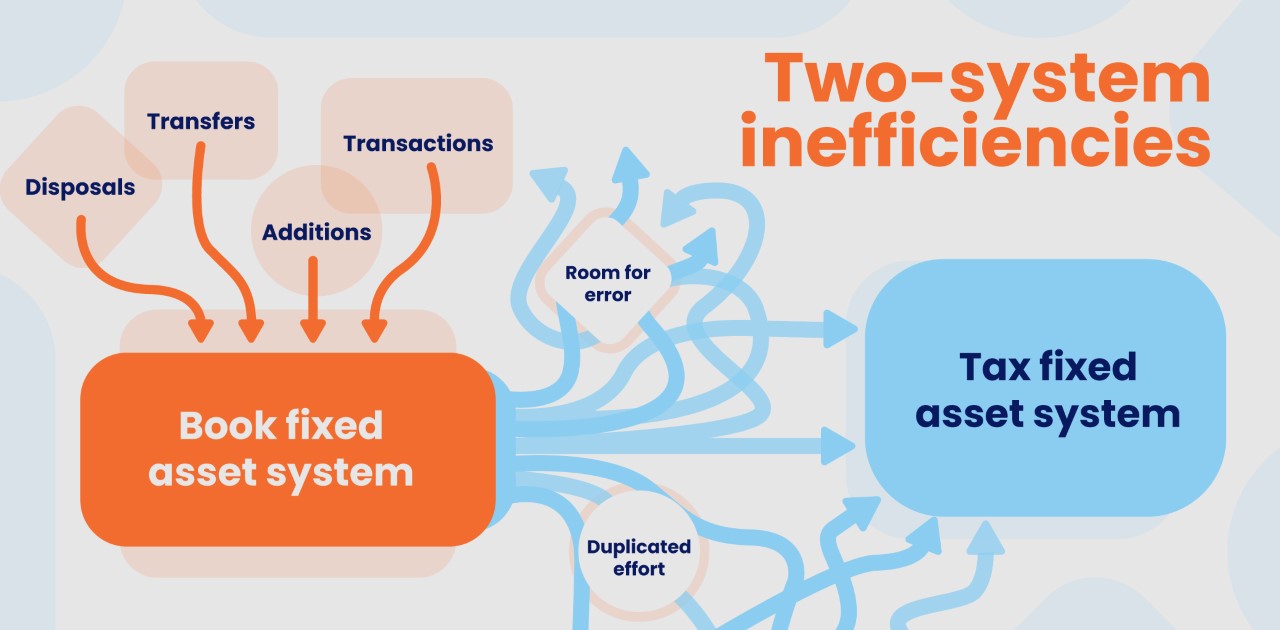

Tax depreciation is calculated with different methods and conventions than book depreciation; however, the underlying assets are usually the same under the two systems. Despite this fact, book and tax assets have historically been stored in two different software systems.

Having integrated book and tax asset records has numerous benefits that you should consider when analyzing a fixed asset system.

Integration reduces the duplication of effort and time it takes to input asset information

Maintaining book and tax asset basis in two separate systems requires all activity in each period to be recorded twice. Additions, disposals, transfers and other asset transactions must be communicated from the book fixed asset system to the tax fixed asset system. Moving information into both systems not only duplicates the time and effort required to account for the assets, this process also increases the likelihood of mistakes due to human error. An integrated system remedies the need to transfer information between systems because updates can be quickly and electronically applied to both asset records, eliminating the risk of human error and saving both time and manual work for the company.

Integration allows for quick reference of asset information during the tax review process

Classification of assets into different tax asset classes requires information about the underlying asset that is usually only stored offline or in the book fixed asset system. This can require significant back and forth between teams to determine the applicable information about the asset. The constant communication can lead to assets being misclassified if the information is not readily available or communication is halted. Having the book and tax record for each asset integrated into the same system allows for quick and convenient reference to the book information to determine the applicable tax classification and treatment. This ease of access increases the likelihood that tax assets are classified correctly and depreciated using applicable depreciation conventions and methods.

Integration saves time and money on tax preparation

During the tax-preparation process, one of the largest book-to-tax differences for many companies is the depreciation adjustment. Calculating this adjustment in different systems requires receiving the book information, analyzing the book information received, applying the changes in book asset information into the tax asset system, validating the tax information, comparing the calculated values for book and tax, reconciling any unexpected differences and then filling out the applicable tax forms. For most tax preparers, the steps of analyzing the book information to make the applicable changes needed to the tax system and validating the tax information is a frustrating and time-consuming process.

Disposals are particularly troublesome when the asset information is present in two different systems. Using the name, acquisition date and any other information present in the book disposal information, tax preparers often have to manually match the book assets to tax assets in their system. Outdated reports and human error could make this process long and grueling. After many hours wasted, if the book asset cannot be matched to a tax asset, a common practice in the profession is to partially dispose of another asset to ensure that the disposal was reflected somewhere on the tax books. This partial disposal would, in turn, cause problems in future years when that asset itself is disposed of and the basis does not match the book record.

Maintaining the book and asset record in one system allows for tax information to be entered on the same record that stores the book information. This eliminates the headache associated with matching book and tax assets during additions, disposals or transfers. Any large variances between book and tax depreciation can be examined and reconciled quickly and effectively, all within one system. By having the information in one place, time and money are saved during the tax-preparation process.

The bottom line

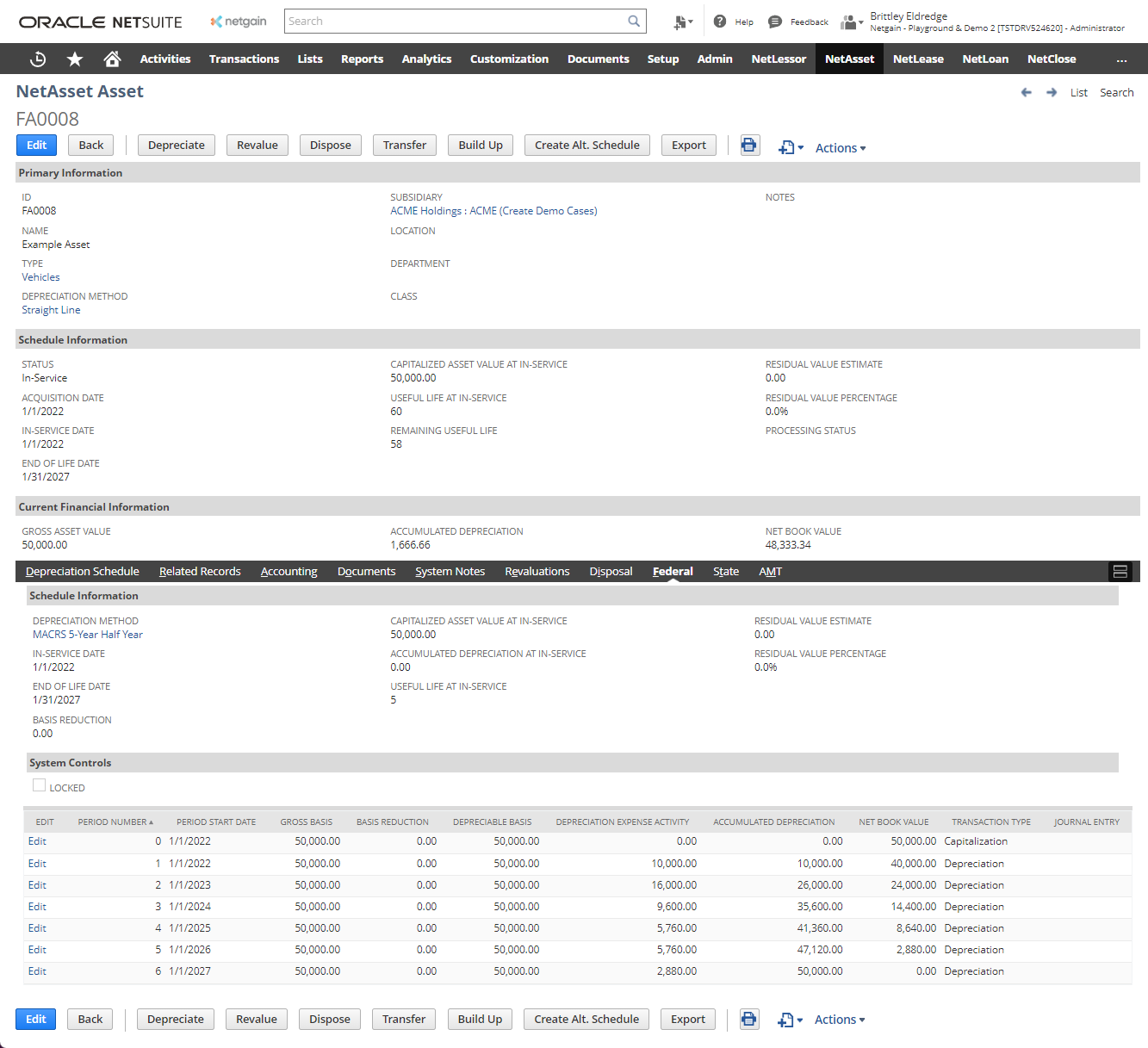

Tax depreciation, despite its easy calculation, can be a time-consuming and frustrating book-to-tax adjustment for many companies and tax preparers. Integrating book and tax asset records into the same system can alleviate much of the manual work that is required to calculate this adjustment and reduce the cost of tax return preparation. Integrated, fixed asset software like NetAsset makes the calculation of one of the biggest expenses on the tax returns easy to compute and convenient to validate.